THE ECONOMIC ENVIRONMENT OF BUSINESS

|

| Spring 2018 |

|

|

Graduate (S) Business Administration 509 THE ECONOMIC ENVIRONMENT OF BUSINESS |

|

|

|

| | HOME | SYLLABUS | CALENDAR | ASSIGNMENTS | ABOUT PROF. GIN | |

|

C. Cost Analysis 1. Cost functions Shows the relationship between costs and output produced a. Fixed vs. variable costs Variable costs -

change with level of output . Fixed costs -

don't vary with output . Semifixed costs - fixed over certain range, variable over others Ex. - Trucks Q = 0 - 5000 => 1 truck Q = 5001 - 10000 => 2 trucks . Ex. - Salaried employees, administrative expenditures .

. . b. Total cost

. c. Average costs AC = average cost = TC / Q

. d. Marginal cost (MC) MC = ΔTC / ΔQ . e. Relationship between average and marginal costs If MC > AC, AC is increasing If MC < AC, AC is decreasing If MC = AC, AC is at a minimum

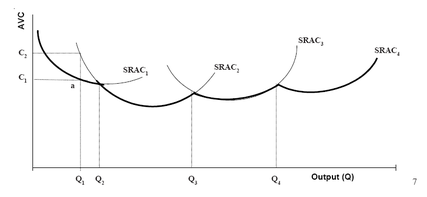

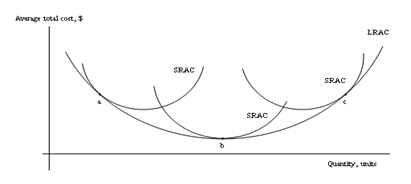

. 2. Short-run vs. long-run costs Short-run - firm cannot change size of production facilities Long-run - firm can adjust plant size, employ alternative technologies .

. Short-run - used to determine day-to-day operational decisions Long-run - used for planning purposes . 3. Sunk vs. avoidable costs Sunk costs - costs incurred no matter what decision is made Avoidable costs - costs can be avoided if certain choices made

. Some fixed costs are not sunk costs . Ex. - Capital that can be transferred to other uses . 4. Profitability a. Economic vs. accounting costs Opportunity cost - cost of foregone alternatives Ex. - Foregone wages, return on capital assets . Accounting costs - only look at costs explicitly incurred Economic costs - include opportunity cost along with accounting costs . Ex. - Quit job to start a business Salary at former job = $200,000 Wages of employees = $300,000 Expenses for supplies and raw materials = $550,000 . Accounting costs = $300,000 + $550,000 = $850,000 Economic costs = $850,000 + $200,000 = $1,050,000 . b. Economic vs. accounting profit Accounting profit (π) = total revenue - accounting costs Economic profit (π) = total revenue - economic costs . Ex. - Quit job to start a business TR = $1,000,000 Accounting π = $1,000,000 - $850,000 = $150,000 Economic π = $1,000,000 - $1,050,000 = -$50,000

Ex. - McDonald's, 2002 Accounting π = $2,113 million Economic π = -$124 million Opportunity cost = $2,237 million Total assets = $23,970.5 million Implied rate of return for alternative use of assets = 9.33% |