B. Trade-offs, Comparative Advantage, and the

Market System

- Scarcity - unlimited wants exceed the limited resources

available to fulfill those wants

1. Production possibilities frontier (PPF)

- Shows the maximum attainable combinations of two

products that may be produced with available resources and current

technology

Ex. - Missiles and wheat

| .................... |

M |

W |

| |

0 |

15 |

| |

1 |

14 |

| |

2 |

12 |

| |

3 |

9 |

| |

4 |

5 |

| |

5 |

0 |

.

.

.

- Opportunity cost -

highest value alternative that must be given up to engage in an

activity

Ex. - Cost of attending USD

.

.

.

- Increasing marginal opportunity costs

- Increasing the production of one good requires

larger and larger decreases in the production of the other

.

.

.

.

.

.

.

.

.

.

- Economy produces increasing quantities of goods and

services

- Due to more resources or technological advances

.

.

.

.

.

.

.

.

.

.

.

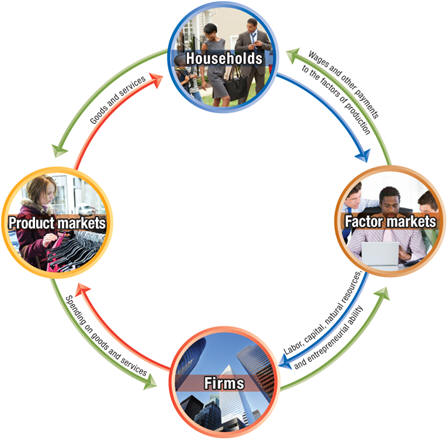

2. The market system

a. Definitions

(1) Market

- Group of buyers and sellers of a good or service

and the institution or arrangement by which they come together for

trade

.

(2) Product markets

- Markets for goods and services

.

(3) Factor markets

- Market for inputs into the production process

.

(4) Factors of production

- Inputs used to make goods and services

.

(a) Labor

.

(b) Capital

.

(c) Natural resources

.

(d) Entrepreneurial ability

- Ability to bring together other factors of

production to produce and sell goods and services

.

b. Circular flow of income

.

c. Market mechanism

- Adam Smith (1776) - An Inquiry into the Nature

and Causes of the Wealth of Nations

- Free market - few

government restrictions on economic activity

- Individuals act in a rational, self-interested way

- Prices send signals about the value of certain

products or activities => leads to the optimal allocation of resources

- Entrepreneurs -

operate businesses, bring together factors of production to produce

goods and services

.

d. Legal basis of market systems

(1) Protection of private property

- Market system requires property to be protected

from seizure by the government or by criminal elements

- Property rights -

rights individuals or firms have to the exclusive use of property,

including the right to buy or sell it

- Guaranteed by 5th and 14th amendments

- Protection of intellectual property

.

(a) Patents

- Protects new products or new ways to produce

products for a period of 20 years

.

(b) Copyrights

- Protects books, films, and software for a period

of 50 years after the death of the creator

.

(2) Enforcement of contracts and property rights

- Contracts must be carried out, private property

must be secure for market system to work

- Legal system used to have rights enforced

- Legal system must be independent from government

and outside forces

|